How Do You Depreciate A New Roof On A Rental Property

How Rental Property Depreciation Works The Benefits To You

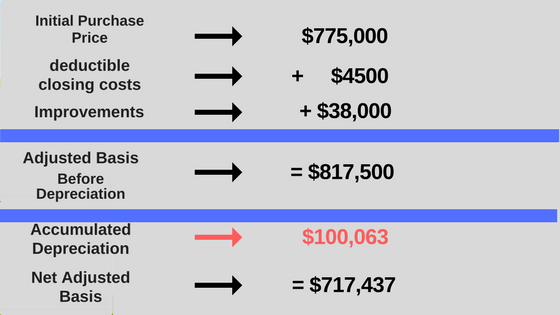

Rental Property Depreciation Rules Schedule Recapture

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

How To Calculate Rental Property Depreciation Morris Invest

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

Rental Property Depreciation Tax Deduction Guide Wealthfit With Images Rental Property Property Rental

Do i keep depreciating a roof on a rental property which has been replaced before its 27 5 life.

How do you depreciate a new roof on a rental property.

How To Maximize Rental Property Depreciation Youtube

Real Estate Investing Frequently Asked Questions Most Common Faqs Real Estate Rentals Renting Out Your House Rental Property

How The New Tax Law Affects Rental Real Estate Owners

How To Calculate Depreciation On Rental Property

Claiming Depreciation On Rental Properties

Mainecoastrealtor Is The Foremost Tax Depreciation Investment Property Service Provider Get Complet Of Schedules T Rental Property Investment Property Property

Confused With Rental Property In Australia For Residential Rental Property You Can Claim A Tax Modern House Plans Diy House Plans Australia House

What Is Rental Property Depreciation

Turbotax Guide To Tax Deductions For Rental Property Depreciation Thestreet

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

Real Estate Tax Depreciation Basics Millionacres

New Tax Law Affects Rental Real Estate Owners Pugh Cpas

The Irs S Dirty Little Secret About Rental Properties By Becky Harding Medium

Tax Depreciation Schedules Australia One Of The Least Benefit Of Property Depreciation Is That They Are Non Cash Deductions It Means Tax Deduction Legal Rule

Why Invest In Real Estate Http Cabpropertiesllc Com Why Invest In Real Estate Real Estate Investing Real Estate Humor Real Estate Marketing

61 Fawcett Street Mayfield Typical Weatherboard Early 20th Century Cottage Mayfield 2304 Nsw Australia Rental Property Investment Property Property

Video What Can You Deduct On Rental Property

If You Re A Real Estate Investor Did You Know That Depreciation Can Actually Be Your Friend When It Comes To Home Refinance Refinance Mortgage Home Equity Loan

1

Canada S Hot Housing Markets Will Help Boost Economic Growth Poll Bnn News Rental Property Real Estate Rental Property Investment

Pdf Download The Landlord S Financial Tool Kit Full Pages By Michael C Thomsett

Everything You Need To Know About Depreciation On Rental Property Investment Property Tips Mashvisor Real Estate Blog

Paying Back Depreciation On A Rental Property Home Guides Sf Gate

How To Deduct A Deck Building A Deck Deck Deck Design

Source : pinterest.com